Advertisement

How to Save ₹1 Lakh in One Year on a ₹30,000 Salary

₹30,000 salary. ₹1 lakh savings target. One year. Is it possible? Yes — here is the exact plan.

The Math First

Monthly salary: ₹30,000. Target savings: ₹1,00,000 per year. Monthly savings needed: ₹8,334 — that means saving 27% of your income every month. Not easy, but completely doable with the right system.

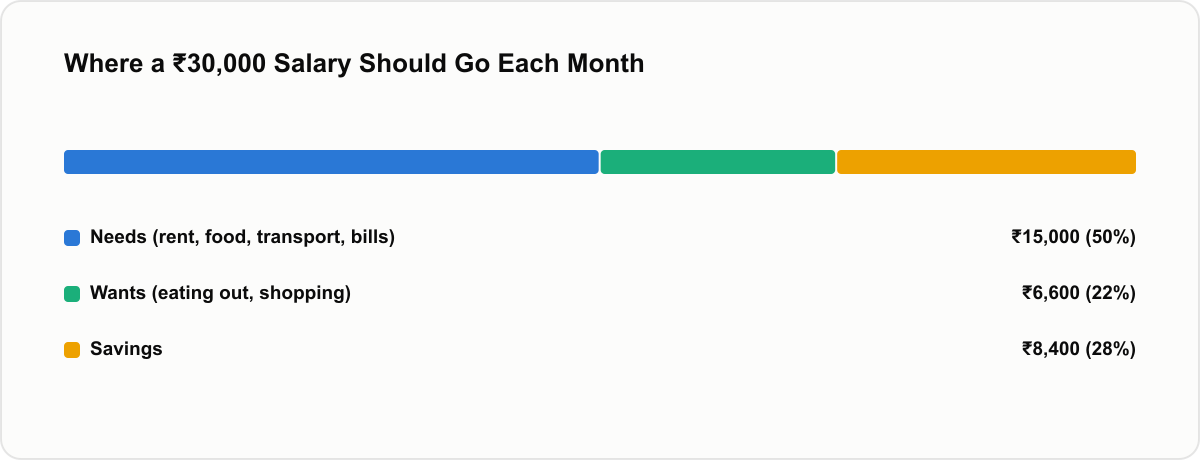

The 50-30-20 Rule — Adjusted for India

The standard rule is 50% needs, 30% wants, 20% savings. For a ₹30,000 salary, adjusted:

- Needs (rent, food, transport, bills): ₹15,000 (50%)

- Wants (eating out, shopping, entertainment): ₹6,600 (22%)

- Savings: ₹8,400 (28%)

Where Most People Leak Money

After tracking expenses of hundreds of people earning ₹25,000-35,000, these are the biggest leaks:

- Food delivery (Swiggy/Zomato): ₹3,000-5,000/month

- Subscriptions forgotten (Netflix, Spotify, Prime): ₹1,000-2,000

- Impulse shopping (sales and offers): ₹2,000-4,000

- Auto/cab instead of public transport: ₹2,000-3,000

- Eating out with colleagues: ₹1,500-3,000

Total leakage: ₹9,500-17,000 per month — that is ₹1.14-2.04 lakhs per year wasted.

The 12-Month Savings Plan

Month 1-2: Foundation

- List every expense from last 3 months

- Cut all unused subscriptions

- Set up a separate savings account

- Automate ₹8,334 transfer on salary day

Month 3-4: Reduce food costs

- Cook at home 5 days per week

- Allow Swiggy only on weekends

- Carry lunch to office 3 days per week

Month 5-6: Transport

- Use metro/bus for daily commute

- Walk for distances under 1.5 km

- Cab only for late nights or emergencies

Month 7-8: Entertainment

- Use free alternatives: YouTube Premium family plan shared

- Movie only once per month

- Free events and parks for weekends

Month 9-10: Income boost

- Start a small skill on Fiverr or Internshala

- Sell unused items on OLX

- Tuition or freelancing on weekends

Month 11-12: Final push

- Review and cut any remaining leaks

- Put bonus or extra income directly into savings

- Do not touch savings account for any reason

Where to Keep Your Savings

Do not keep savings in your salary account — you will spend it. Better options:

- SBI/HDFC Savings account (separate, no debit card linked): 2.7-3% interest

- Recurring Deposit: 5-6.5% interest, auto-deducted monthly

- Liquid Mutual Fund (Paytm Money or Zerodha Coin): 6-7% returns, withdraw anytime

Avoid Fixed Deposits for short-term savings — they carry a penalty for early withdrawal.

Quick Wins to Start This Week

- Monday: Cancel all subscriptions you have not used in 30 days

- Tuesday: Cook at home for the entire week

- Wednesday: Walk or take public transport instead of cab

- Thursday: Pack lunch for office

- Friday: Transfer ₹2,000 to savings account right now

Those 5 actions alone will save you ₹3,000-5,000 this month.

Reality Check

Saving ₹1 lakh on a ₹30,000 salary requires real sacrifices. You will miss some eating out. You will cook more. You will take the metro when you want to take Uber. But at the end of 12 months, you will have ₹1 lakh in savings — a real financial cushion that most people your age do not have. That cushion changes how you feel about your job, your life, and your future decisions. Start today: save the first ₹500 right now.

Frequently Asked Questions

Advertisement

Was this article helpful?

Advertisement

Comments

No comments yet. Be the first to share your thoughts!

Related Posts

Zero-Based Budgeting: A Practical Guide to Giving Every Rupee a Job

The budgeting method that forces you to plan discretionary spending before you make it

Zero-based budgeting assigns every rupee of income a job before the month starts. A step-by-step method for setting one up, with a worked example.

How to Build an Emergency Fund From Scratch, Whatever Your Income

Four milestones that work whether you're saving ₹500 or ₹15,000 a month

An emergency fund turns a crisis into an inconvenience. Four concrete milestones for building one from zero, where to keep it, and how to fund it on a tight budget.